Applying for and opening a new credit card can be exciting because it usually follows up with a welcome bonus after meeting the spending requirement.

At the end of every billing cycle, you receive a statement, which is money owed to the issuer, and paying the balance in full and on time is greatly stressed here at TPG.

However, what happens when you close a credit card with a balance? Is it forgotten in the wind, or can it hurt your credit score and affect future borrowing needs?

Today, we’ll explore if you can close a credit card with a balance or if you should close it with a zero balance instead.

Pay off a credit card or maintain a balance?

To avoid interest charges, it’s best practice to pay off the credit card balance each month. When carrying a balance month to month, interest charges begin to accrue, diminishing the value you receive from a card, such as cash back and rewards points.

That said, you may maintain a balance on your credit card as long as you pay off the statement balance. That’s because the current balance on a credit card is not subject to interest charges until that month’s billing cycle ends.

Can you close a credit card with a balance?

Closing a credit card with a balance is possible. However, there are some things to keep in mind.

When you close a credit card, you can no longer make purchases on the credit card and also forfeit transferable rewards points. Upon closing a credit card with a balance, you remain responsible for the balance and will continue to accrue interest on it while receiving billing statements.

If you are determined to close a credit card, it’s better to pay off any current balance before doing so to avoid late fees, interest charges and the possibility of the debt being sent to collections if left unresolved. If the card has no annual fee, you’re better off leaving the account open and leaving it for emergency use, whereas if it does have an annual fee, you can consider downgrading to a no-annual-fee card.

Daily Newsletter

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

Another alternative to closing a card with a balance is to transfer the balance to an existing or new credit card. By transferring the balance on the card you wish to close, you can avoid paying a lump sum of the balance and avoid interest fees for a promotional period.

Check out TPG’s best balance transfer credit cards to see how to take advantage of great offers.

Related: The best way to pay credit card bills

Impact of closing a credit card with a balance

Closing a credit card with a balance can hurt you in several ways, including negatively affecting your credit score and overall credit report.

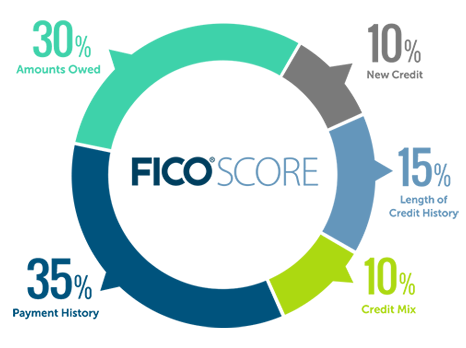

When closing a credit card, you reduce the length of your credit history and the average age of your accounts. Length of credit history makes up 15% of your FICO score, so expect a dip when you close a credit card.

If you close a credit card with a balance, you also increase your credit utilization, as this reduces your overall credit across all accounts. If the closing of a credit card pushes your utilization over 30% of the total available credit, you risk negatively affecting your credit score. If you close a card due to a history of late payments, know that such incidents remain on your credit report for about seven years.

Closing a credit card with a balance can also affect you long term if you do not pay off the balance promptly. You’ll continue to receive billing statements for any balances owed to the issuer.

If the balance remains unresolved for some time, the issuer can send it to a collections agency, which will be reported to the three credit bureaus, negatively affecting your creditworthiness in a major way.

Bottom line

It is possible to close a credit card with a balance. However, despite closing the account, you are still responsible for paying the balance and any associated late or interest fees. A better move is to pay off the entire balance of a credit card before closing the account.

If you can avoid closing a card by downgrading it to a no-annual-fee card or shifting its line of credit to another card with the same issuer, you may be able to protect your credit score and avoid dealing with future interest charges or negative marks on your credit report.