Credit card debt in the U.S. has reached an all-time high, breaking the $1 trillion mark for the first time. According to the New York Federal Reserve‘s latest report on household debt and credit, credit card balances increased by $45 billion (4.6% quarterly increase) in the second quarter of 2023 and now stand at $1.03 trillion.

Here at TPG, we spend much of our time going on about the incredible value you can get from credit card rewards, whether you’re looking for free flights, hotel stays or simply some cash back to pad your bottom line.

However, these recommendations all carry a huge disclaimer: If you get into credit card debt, you’ll rapidly erase the value of any rewards you’ve earned and end up in a difficult financial situation.

Today, we will look at what you need to know about how to pay off credit card debt and avoid acquiring more in the future.

The minimum payment problem

If you have credit card debt, you’re not alone. Americans have an average credit card debt of $5,589, according to Experian. As interest rates remain high, it’s more important now than ever to understand and work to pay off credit card debt.

Credit card debt is easy to acquire because of credit cards’ high interest rates for unpaid balances, especially on the most rewarding cards. The other two types of most common debt are mortgages and car payments, which currently have average interest rates of over 6%. In contrast, the average interest rate for a new credit card account is over 20%.

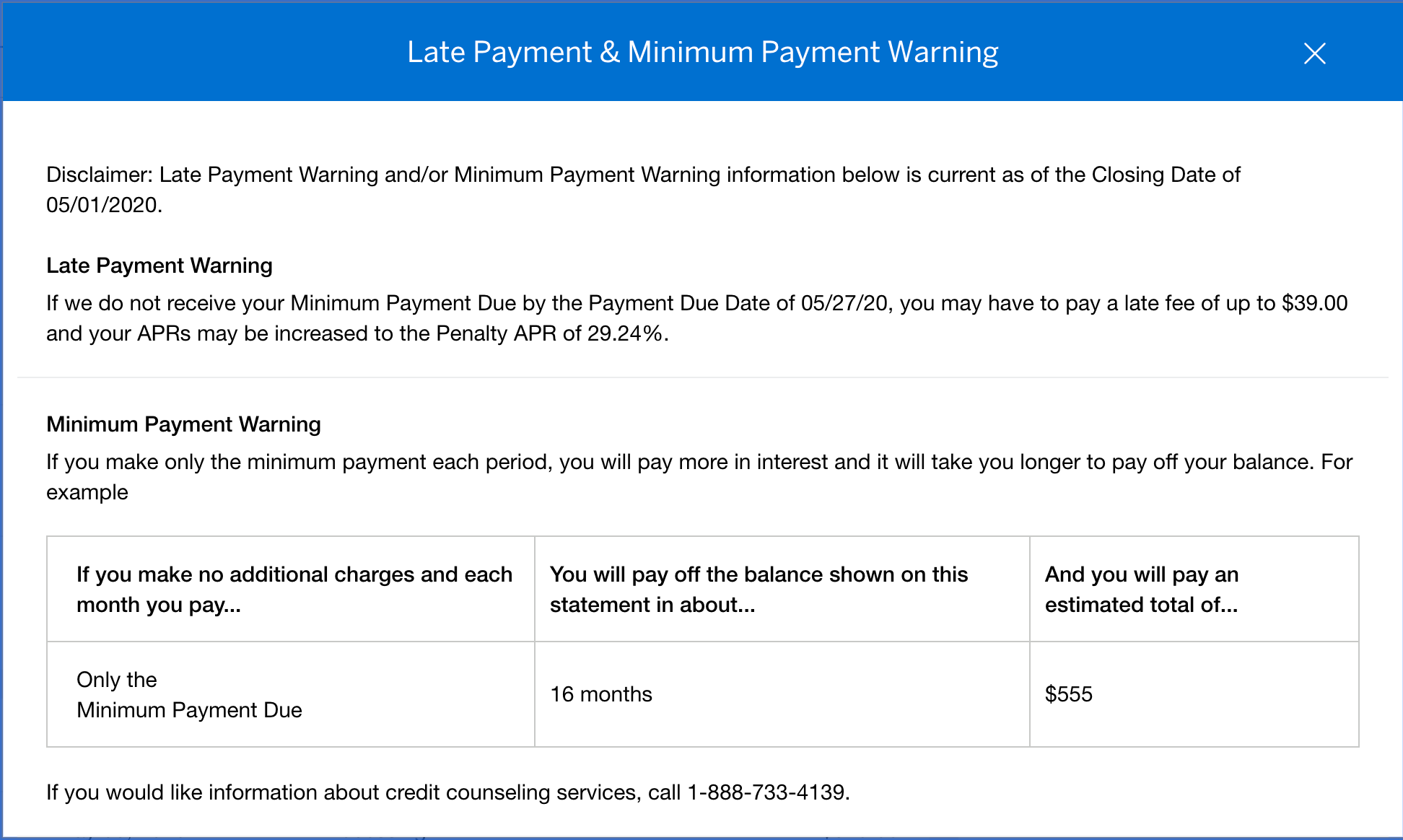

Thankfully, strong consumer protection laws in the U.S. require card issuers to help you understand the dangers of credit card debt. At the end of each monthly billing cycle, your credit card issuer sends you a statement showing all the changes you made during that billing cycle. This statement shows the total amount you owe as of the statement closing date (your statement balance) and also shows a “minimum payment” due.

If you pay your statement balance in full every month, you never have to worry about racking up credit card debt. But if you only make the minimum payment (or any amount below the full statement balance), you will start accruing interest and it can become an issue.

Related: Tip: Amex’s ‘Please Pay By’ date isn’t the same as your payment due date

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts.

For example, this is a Marriott Bonvoy Business® American Express® Card statement for a balance of $375. If the cardholder pays off the card in full before the payment due date, they do not have to worry about paying interest.

However, the statement outlines the amount of time and money it would take them to pay off this balance if they were to only make the minimum payment of $35. If they made that choice, it would take them 16 months and cost them an extra $180 in interest charges to pay just this card off. If they were late on their payment or paid only the minimum amount on other months, they would owe even more.

Related: Does carrying a balance help my credit score?

How to pay off credit card debt

Lower spending habits

Before you start tackling debt, take a look at your spending habits. Identify areas where you can cut back. The more you limit your spending, the more you can put toward your debt payment.

List out debts

This can be difficult to face, but it is an important element of choosing your approach. Make a list of each debt you have and its interest rate.

Choose an approach

There are a few approaches you can take if you want to pay off credit card debt.

- Avalanche method: First, pay off the card with the highest interest. Take the money you were able to cut from your spending and put it toward paying down this card. When you have paid this debt, move to the debt with the second highest rate. Continue until you have eliminated your credit card debt.

- Snowball method: Focus on your debt with the smallest balance first. When you have paid it off, use that money to work toward your next smallest balance. Eventually, use this momentum to tackle your debt with the highest balance and you will eliminate all of your credit card debt.

- Consolidate credit card debt: You can also consolidate your credit card debt by opening up a new credit card with a 0% intro annual percentage rate (APR) offer or take advantage of balance transfer offers. The exact offers vary from card to card, but you can transfer your high-interest balance to this new card and pay it off over the course of 12 to 15 months without racking up any more interest. Just make sure to pay off the balance before the 0% intro APR period expires or you’ll end up fighting an uphill battle against interest again.

- Credit card forgiveness: It’s unlikely that a bank will outright forgive your credit card debt, but you might be able to negotiate a lower interest rate or monthly payment plan. There is no guarantee, but it doesn’t hurt to ask.

Related: 5 tips to make a successful balance transfer

How to avoid credit card debt moving forward

When you are out of credit card debt, put strategies in place to make sure you stay out. You can use several tools to your advantage, starting with autopay. Most major credit card issuers allow you to set up autopay on your accounts, meaning your bills will automatically be paid before the due date and you’ll never miss a payment. You can use this updated envelope system to ensure you have enough money in your bank account to avoid overdraft fees.

Another option is to pay off all of your balances every two weeks. To do this, set a recurring reminder on your calendar for the 1st and 15th of every month. When that reminder pops up, log in and pay off all your balances, even if the statement hasn’t closed yet. Since you usually have about a month from when your statement closes to when your bill is due, this every-two-week method helps you stay ahead of your bills and never miss a payment.

Related: Ten Commandments of credit card rewards

Bottom line

No matter where you fall compared to Americans’ average credit card debt, plenty of strategies are available to help you pay off whatever credit card debt you might have.

While you shouldn’t hold your breath for credit card debt forgiveness, you can consolidate credit card debt or use one of a few different approaches to pay it off, like the avalanche method.

Regardless of which route you choose, be sure to put a plan in place to avoid or reduce credit card debt in the future.

Related: How to earn points and miles with fair to poor credit

Additional reporting by Ryan Wilcox, Ethan Steinberg and Chris Dong.