Sometimes life happens, and it can get you off track financially.

You can have a financial plan, budget and adequate savings. Still, it may not be enough for you to avoid missing payments and letting your accounts go delinquent.

Credit card delinquency isn’t anything new, so let’s take a closer look at what exactly it is — and how you can avoid it.

What is credit card delinquency?

In a 2023 FICO Report, 11% of U.S. adults admitted to having missed a credit card payment. These late or missed bill payments begin the process of credit card delinquency.

Delinquency doesn’t mean that you haven’t paid your balance in full; it simply means you didn’t make the required minimum payment. However, at TPG, we always recommend paying in full to avoid interest on your balance. This is one of TPG’s commandments of credit card rewards.

A 2023 Philadelphia Federal Reserve report showed that credit card delinquency is at an all-time high.

The rising rates may suggest credit card companies are working with more risky borrowers — and that was even before the coronavirus pandemic. Because of this, some banks may cut credit limits for cardholders and be cautious when accepting new cardholders.

Failure to pay bills on time can result in credit card suspensions, revocations, or even a charge-off; additionally, you can be assessed late penalties and fees on delinquent accounts.

Let’s go over what all of that means by walking through the days and months after missing a payment.

Daily Newsletter

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

The beginning stages of card delinquency

If you miss a payment deadline, usually within 30 days, little happens to your account. Your credit card company may issue a late payment fee, but if you are able to get your account current within this time period, this negative mark should not even show up on your credit report. Additionally, if you aren’t a repeat offender when it comes to missing payments, your bank may waive a late payment fee if you ask nicely.

After the 30-day mark of a missed payment, your account will likely be reported to all three credit bureaus as delinquent. This means that it usually takes two consecutive missed payments for delinquency to start to seriously impact you. Consumers get a bit of a buffer before dealing with significant repercussions.

The creditor may also temporarily suspend or pause your account and stop authorizing purchases for payment.

The middle stages of card delinquency

After several months in delinquency (usually three to four months late), credit card companies are likely to drop the hammer and completely suspend your account and require certain actions to reverse a suspension.

If you’re dealing with extenuating circumstances such as a job loss, or other financial hardship, you can contact your card issuer about potential custom repayment options. Banks may be more willing to work with you, especially if you’re going through difficult economic times.

Besides working with the issuer directly, you could also work with a nonprofit credit counselor who may be able to help create a debt management plan. Keep in mind the counselor has to work with you and the creditor and be agreed upon by both parties.

The later stages of card delinquency

Eventually, your card will be revoked and you can never use it again, even if you make a payment in full. This usually happens around the four- to five-month mark.

If you still haven’t made progress on your account to bring it up to date, the credit card issuer may conduct a “charge off” as the final stage of delinquency. This typically occurs after six months past due.

From an accounting perspective, this simply means the issuer has recategorized the debt from an asset to a loss. However, a charge-off has serious implications for your credit, and you will still need to pay back your balance in full.

Related: A complete guide to credit card debt

The effects of delinquency on your credit

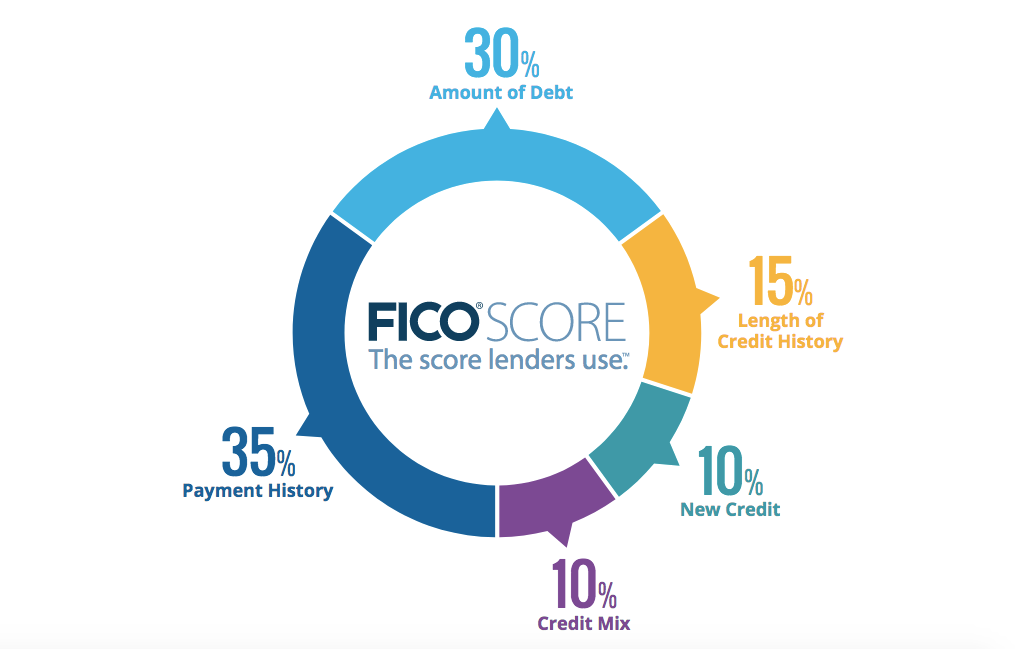

Now that we’ve discussed what delinquency is, how badly does it affect your credit? The credit score factors of payment history and amount owed are most affected when you miss payments.

Payment history

Not paying your bills on time impacts your payment history, which makes up 35% of your FICO score.

Amount owed

Next, a credit card revocation (this is when the issuer closes your account) can negatively influence your credit utilization ratio. With less overall available credit, your utilization ratio increases. “Amount owed” is about 30% of your credit score, so this also will be negatively affected.

Charge-off

Finally, a credit card charge-off will remain on your credit report for up to seven years. The exact impact on your credit score varies, but a charge-off has the potential to seriously affect your financial future.

How to avoid credit card delinquency (and a charge-off)

Make all payments on time. Making at least a minimum payment on your card’s bill every month will avoid delinquency. One strategy to do this is by setting up autopay. This will keep you from forgetting about a balance entirely.

Don’t spend on your card. This might seem the most obvious, but if you’re at risk of missing a payment, don’t continue spending on the card.

Call your credit card company if you’re struggling. Card companies may be willing to work with you for extended payment options or other ways to help keep your balance current.

Related: The biggest factors that impact your credit score

Bottom line

There’s a big difference between one late payment by a few days and a delinquent account that goes unpaid for months. The good news is that there are ways to get back in good standing with your card issuer before things start turning ugly.

Of course, it’s easy for late payments — plus the interest on your revolving balance and other fees — to quickly add up. It can snowball out of control. That’s why it’s crucial to not only bring your accounts current as soon as possible but also to try to avoid getting into the situation in the first place.

However, it’s sometimes unavoidable, especially for those in financial hardship. Knowledge is power, though, and with these tips, you’ll know what to look out for and what to do to avoid delinquency.