A common question we get from beginners is about the difference between a “soft pull” and a “hard pull” on your credit report.

Both terms are frequently used when discussing applying for new credit cards, but how does each affect your credit score?

The major difference between the two is that a hard pull appears on your credit report while a soft pull does not. Let’s dig deeper.

What is a hard pull?

When you apply for a line of credit, whether it be a new credit card, mortgage, auto loan or some other type of loan, the lender will pull your credit report from at least one of the three major credit reporting agencies — Equifax, Experian and TransUnion. This is called a hard pull or a hard inquiry.

These checks are tied to an application and will appear on your credit report. That means they could potentially affect your score since new inquiries on your credit report are a factor in determining your credit score. What is considered an official application? Any time you send in a request for a line of credit and share your full identification details, such as your name, address and Social Security Number.

A hard pull results in the lender obtaining your official credit report and credit score from whichever bureau it requested the information. This is a much more in-depth look at your credit history than what might be collected and sent over after a soft pull.

When are hard pulls performed?

As mentioned above, hard pulls are almost always connected to an application for credit of some sort. Credit card issuers generally run hard pulls when you apply for a new card (though there are some exceptions to this). Mortgage and private student loan lenders will also run a hard pull on your credit. Occasionally, a potential landlord may ask to perform a credit check. Depending on what service they use to run that check, it may result in a hard pull.

Lenders will want a deeper look at your credit report to ensure you are a responsible borrower and likely to repay the amount of credit you request.

Related: Ultimate guide to credit card application restrictions

Daily Newsletter

Rewarding reading in less than 5 minutes

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

What is a soft pull?

A soft inquiry does not appear on your credit report and does not affect your score at all. Soft pulls generally occur when you check your credit score or you give someone, like a potential employer, permission to review your credit report.

Generally speaking, a soft pull won’t result in someone receiving your full credit profile and score. Instead, they might get an estimated score based on the information requested or may get limited information on just one area of your report.

These credit checks are not tied directly to a credit application of any kind, which is why they aren’t recorded in your report and do not affect your credit score.

When are soft pulls performed?

Any time you or someone you give permission to check your credit score and it isn’t tied to an official application, it will likely result in a soft pull. Generally, a soft pull won’t result in a full, in-depth report being shared with the recipient.

For example, checking your credit through a service such as Credit Karma results in a soft pull. Additionally, when insurance companies request a credit check to give you a quote, that will usually also result in a soft pull.

While opening new credit accounts results in a hard pull, looking at pre-qualified offers generally only requires a soft pull. Card issuers or other lenders may offer to perform one to give you insight into your approval odds before you submit an official application.

If you are working to improve your credit score and are wary of any nonessential hard inquiries being listed on your account, pre-qualification tools that don’t affect your credit score at all can be useful. Additionally, you can use pre-qualification tools such as CardMatch to find the best welcome offers available across certain credit cards with targeted offers.

How do hard pulls affect your credit score?

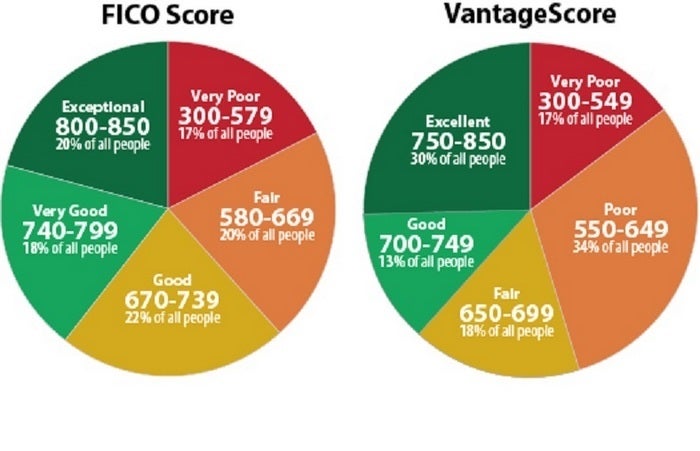

Hard pulls on your credit report signal that you want to open a line of credit. The more inquiries you have in a short period of time, the more creditors might assume you are in financial distress and, therefore, at a higher risk for delinquencies. Both the FICO and VantageScore credit scoring models factor in recent credit behavior, including new inquiries. This can affect your score in two ways.

When you apply for a new account, you may notice a slight dip in your score because of the hard pull. This is almost always temporary and should only affect your score by a few points at most.

However, if you have opened many new credit accounts recently, that could affect your score in the long term. Hard inquiries can stay on your credit report for up to two years, which means that’s how long they can potentially affect your score.

Hard pulls also factor into your Chase 5/24 eligibility.

Related: What is a good credit score?

How many hard pulls are too many?

According to Credit Karma’s credit score service, keeping recent inquiries below two is optimal. You start to drift into the “red zone” once you have five or more on your account.

Take this with a grain of salt, though. FICO only uses new inquiries to make up 10% of your score, and TransUnion lists credit behavior and new accounts as a “less influential” factor. Many TPG staffers have seven or eight inquiries on their reports and still have excellent credit scores.

While you’ll want to avoid unnecessary inquiries on your account, don’t let the possibility of having another hard pull on your report stop you from applying for a new credit card if your score is otherwise healthy.

Related: Should I apply for a credit card now?

Bottom line

Your credit score and overall credit report are both important to your financial health. Knowing the difference between a hard pull and a soft pull can help you mitigate the risk of dinging your score and give you peace of mind that checking your score or going through a pre-qualification tool won’t affect it.

Remember that while hard inquiries can affect your credit score, they only make up a small percentage of your overall score. As long as you have a proven history of paying bills on time and not overutilizing your lines of credit, a new inquiry shouldn’t negatively affect your score in the long term.

Additional reporting by Danyal Ahmed, Stella Shon and Benét J. Wilson.