Some credit cards offer car rental insurance when you use your card to pay for a rental. The insurance covers the vehicle if you’re in an accident or the car is stolen or damaged.

A small number of premium travel rewards credit cards even offer primary coverage, meaning you don’t have to file with any other insurance first, but secondary coverage is much more common.

While most American Express credit cards don’t automatically offer primary car rental coverage, most will allow you to purchase a Premium Car Rental Protection policy that provides primary coverage.

For a small fee, the optional Premium Car Rental Protection policy can be added to rentals booked using an eligible Amex card. We explore this optional coverage and let you know when it makes sense to enroll.

What car rental protection is automatically provided by American Express cards?

Most eligible American Express cards offer secondary car rental loss and damage insurance that covers you when an eligible rental car is damaged or stolen.

However, since the insurance is secondary, if something happens to your rental vehicle, you must file a claim with your primary insurer (such as your personal car or travel insurance) before submitting a claim to Amex.

This is less than ideal, as it can raise your insurance premiums. It can also be problematic if you have a high deductible on your primary policy, as it could leave you out of pocket for hundreds or even thousands of dollars.

That’s why it’s a good idea to try and obtain primary rental car insurance whenever possible.

If you carry an Amex card and are eligible for secondary insurance, beware that some vehicles are excluded from coverage. These include:

Daily Newsletter

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

- Cargo vans

- Custom vans

- Vans with a seating capacity of over eight passengers

- Cube vans

- Box trucks

- Any truck that has a gross vehicle weight rating of 10,000 pounds or more

- Antique cars

- Limousines

- Off-road vehicles

- Motorcycles

- Mopeds

- Recreational vehicles

- Motorized carts

- Campers

Additionally, any rental vehicle rented in Australia, Italy, New Zealand or any country on the Office of Foreign Assets Control sanctioned country list is excluded.

If you want to know whether a particular American Express card provides secondary coverage, the Amex website displays policies for all cards that include this coverage.

Different cards provide different levels of coverage, so be sure to check the policy for your particular card.

Related: The 10 cards we think Amex may refresh this year — here’s what to expect

What is American Express Premium Car Rental Protection?

American Express Premium Car Rental Protection offers primary insurance coverage for damage to or theft of your rental vehicle. It applies to a wide range of rental car types, including luxury vehicles, pickup trucks and SUVs.

The coverage, good for up to 42 consecutive days, can be used to insure rental cars in most countries worldwide, with a few exceptions.

As mentioned, most American Express cards — even those that don’t include secondary coverage on rental cars — allow you to purchase this primary coverage at a reasonable flat cost per rental.

Primary coverage means you don’t have to file with any other insurance provider before filing with American Express. Enrollment is required for select benefits.

Remember, though, the included secondary car rental policies differ across American Express cards, so yours might not be exactly like another Amex offering.

What is excluded from Premium Car Rental Protection coverage?

Even with Premium Car Rental Protection, rentals longer than 42 consecutive days (30 consecutive days for Washington state residents), as well as the following rental types, are excluded:

- Any truck other than a pickup truck

- Cube vans or box trucks

- Leased or mini-leased vehicles

- Vehicles that, after manufactured by the maker, have had any part customized or modified (except for driver’s assistance equipment for a physically challenged driver)

- Vehicles for hire or commercial purposes

- Antique cars (any vehicle more than 20 years old or that has not been manufactured for 10 or more years)

- Limousines, off-road vehicles, motorcycles, motorbikes, mopeds, recreational vehicles, any motorized cart (including golf carts), moving trucks or moving vans, campers or trailers

Additionally, you won’t be covered for:

- Costs attributed to the rental company’s normal course of doing business and expenses assumed, waived or paid for by the rental company or its insurer

- Damage that has occurred before possession of the rental car

- Tires, unless other damage occurs to the rental car from the same accident or theft of the entire rental car occurs

- Defects in the manufacture of the rental car

- Diminished value, unless required by law

- Depreciation, unless reimbursement for depreciation is required by law

- Wear and tear, including such effects caused gradually over time

- Any property other than the rental car and personal property

- Lost items

- Animals, furniture, art, money, securities, tickets or documents

- Items left in the rental car after the cardmember or authorized driver has relinquished possession

- Any injury, except coverage for a covered person described under the accidental injury expense benefit and accidental death or

dismemberment benefit - Any injury or physical condition of a covered person existing before an accident

And benefits will not be paid if the loss for which coverage is sought was contributed to or caused by any of the following:

- Violation of the rental agreement with the rental company

- Acts by a covered person to intentionally damage or injure

- Consumption of alcohol at or in excess of the legal blood alcohol level for operating a motor vehicle in the state or locality in which the accident occurred

- Being under the influence of any drug unless taken as prescribed or administered on the advice of a physician or dentist

- War or act of war, whether declared or undeclared

- Actual, alleged or threatened discharge, dispersal, seepage, migration, escape, release of or exposure to any hazardous biological, chemical, nuclear or radioactive material, gas, matter or contamination

- Confiscation by a governmental authority

- Freezing and mechanical breakdown or electrical failure, except where it results from theft

- The rental car being left unattended and unlocked or a window not completely closed

- Pushing or towing anything

- Violation of criminal law or commission of a criminal act, whether cited or charged, by or on behalf of the covered person

- Participation in a riot, civil disturbance or insurrection

- Suicide, attempted suicide or intentionally self-inflicted injury while sane

- Failure of the cardmember or authorized driver to surrender all the vehicle keys following possession

- A rental car used outside the rental territory authorized by the rental company

- A rental car used for any manner of racing or team sport

- A rental car used for hire, whether for hire to carry persons or property

- Off-road operation of the rental car

- Any disease, illness or infirmity

What cards are eligible for Premium Car Rental Protection?

Most American Express cards can be enrolled in the Premium Car Rental Protection program.

However, corporate cards (which are different from business credit cards) and card accounts issued by a third-party bank partner of American Express are typically not eligible.

Additionally, eligibility may vary by your state of residence and the enrollment status of other card accounts you previously opened.

How do I enroll in Premium Car Rental Protection?

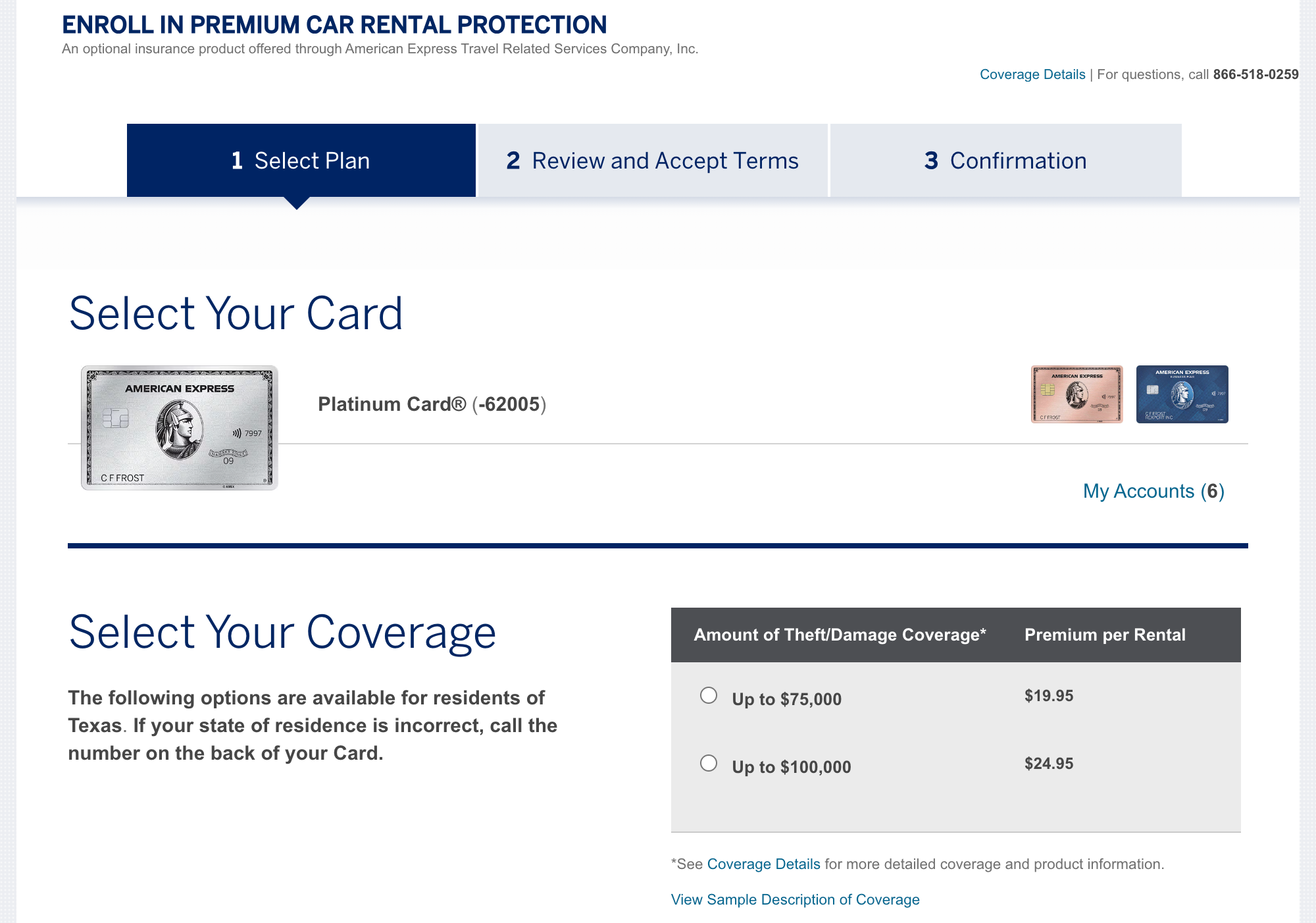

To enroll, visit the American Express Premium Car Rental Protection page and click “Enroll Now.” You’ll need to log into your American Express account, select the card you want to enroll, choose the plan you’d like and review the program’s terms and conditions.

You can enroll cards online for which you are the primary cardholder, but you must call 1-866-518-0259 to enroll authorized user cards.

You won’t be charged anything until you use an enrolled card to rent a car, at which point the premium will automatically be posted to your account. You’ll remain enrolled until you explicitly terminate your enrollment.

So, if coverage isn’t necessary for a specific car rental reservation, terminate your enrollment before the rental by calling the same number as above (1-866-518-0259) or the number on the back of your card.

If you don’t cancel, you’ll continue to be charged for coverage each time you rent a vehicle using an enrolled card.

Reasons to enroll in Premium Car Rental Protection

Although the American Express Premium Car Rental Protection policy isn’t expensive, it’s usually better to use a card that automatically provides primary car rental protection when you use that card to pay for a rental.

However, there are some reasons why you might want to use an American Express card and enroll in the Premium Car Rental Protection program instead:

- None of your credit cards offer primary car rental loss/damage insurance

- You’re renting a pickup truck, cargo van, passenger van or SUV and none of your cards offering primary car rental insurance cover this type of vehicle

- You need to rent a vehicle for up to 42 days and none of your cards offering primary insurance cover a rental of the length you need

- You value the medical expense and property loss benefit, both of which provide secondary coverage but aren’t included in the benefits provided by most credit cards

- You want or need to use an American Express card, perhaps due to better points earning, an Amex Offer or a claims process that many readers have said is more straightforward than filing claims through other issuers’ benefits administrators

Related: Hitting the road this summer? Here’s everything you need to know about rental car elite status

How to file an Amex Premium Car Rental Protection claim

If something does go wrong while you’re on the road, here’s what you need to do to take advantage of American Express Premium Car Rental Protection.

Your first step should be to report any damage to your rental car — including vandalism, theft or an accident — to the appropriate law enforcement agency as soon as reasonably possible.

Next, call your rental agency to inform them of what has happened, that you have notified the authorities and that you will be filing a claim through American Express.

Then, call the number on the back of your enrolled card to report the incident and begin the claims process.

You’ll be sent a claim form if required. This form and all other requested documentation must be returned to the Premium Car Rental Protection Claims Unit within 60 days following the date of the damage or theft.

Coverage may be denied if the required documentation is not received within 60 days of the date of loss — except for documentation that has not been furnished for reasons beyond your control.

Required documentation may consist of but is not limited to:

- Itemized bill for repair or replacement of the rental car or item

- Report from law enforcement agency, such as a police report

- Photos of the damaged vehicle

- Copy of all claim documents and correspondence provided by the rental company

- Copy of the written rental agreement with the rental company

- Death certificate and/or itemized medical bills and medical records

- Signed authorization to obtain medical records

- Completed claim form

- Documentation from the rental company indicating that the covered person was responsible for the damages or loss

- Receipts or proof of ownership for the stolen or damaged item

If your claim is approved, it will be payable to the cardmember or rental agency, depending on the circumstances and coverage.

Is Amex Premium Car Rental Protection worth it?

The American Express Premium Car Rental Protection policy provides cardmembers with a solid option for insuring their rented vehicle.

Competing travel cards from brands such as Chase include primary car rental insurance by simply using the credit card to pay for the rental.

However, note that the third-party insurance provider that Chase and some other issuers, such as Capital One, use has a poor reputation for accepting claims.

If you don’t have a card that provides primary auto rental coverage in your wallet, then the American Express Premium Car Rental Protection policy can be a great choice for a reasonable fee.

It’s also a good option if you’re booking a longer rental or vehicle that’s otherwise difficult to insure, such as a pickup truck, van or SUV.

Bottom line

If you’re a frequent traveler, having a credit card that offers car rental insurance can be worthwhile. However, most credit cards only offer secondary car rental loss and damage insurance, so you must first file a claim with your primary insurer if your rental car is damaged or stolen.

If you have an eligible card, the primary coverage offered with Amex’s Premium Car Rental Protection can provide some additional peace of mind.

Related reading: